“Passive Income”

In other words, invest in assets and make money for free while you sleep.

To the new investor, the idea itself may seem ridiculous. But for weathered tycoons, this feeling is the driving force behind massive oceans of wealth.

Of course, there are so many investment opportunities to choose from today – from more traditional routes like real estate REITs and stock market indices to newer head-turners like Bitcoin and Tesla.

But the question remains.

Which one has had the best returns so far?

In today’s article, we’re going to look at how much you would have made if you had invested $ 10,000 in one of these asset classes two years ago.

Singapore REITs

As we all know, $ 10,000 is not enough to get you a toilet in Singapore Real Estate (let alone a whole unit).

Fortunately, for those of us with smaller capitals, REITs (or Real Estate Investment Trusts) exist.

They are essentially a portfolio of properties that large companies (think capital and) buy, operate and manage – all with their investors’ money.

These REITs typically generate solid dividends of between 3 and 8 percent per year (paid quarterly / semi-annually).

Of course, just like individual stocks, these REIT valuations have been subject to decline and increase over the years – with the recent decline in the Covid-19 market (and the rebound that followed) being no exception.

There are also different REITS in different sectors (retail, trade, industrial, logistics, hospitality) – but for today’s article we are only looking at this one REIT with the highest returns made in the last 2 years.

Keppel DC REIT

Since REITs are so dependent on dividend yields, it would be fatal to ignore the total dividend yields over this 2 year period.

So, I took into account both capital gains and dividends paid during that period to determine the REIT with the highest payout.

However, it appears that the total capital gains for our REIT of the day far outweigh the total dividend yields.

Here are the calculations in brief (don’t hesitate to jump to the end).

Assuming I had invested $ 10,000 in the Keppel DC REIT when the market opened on February 15, 2019, I would hypothetically have bought 7,022 shares at ~ $ 1.42 each.

That would be up to $ 9998.63.

Over the next 2 years, we would be making 5 dividend payouts of $ 1,171.11 ($ 265.47 + $ 124.80 + $ 136.93 + $ 307.21 + $ 336.70).

In terms of actual capital gains, I would hypothetically have made a whopping $ 20,574.46 if I had sold my 7,022 shares on February 15, 2021 at a market price of ~ $ 2.93 each.

Total = $ 21,745.57 (up 117.49 percent)

(Note: in most cases, stock valuations go down after the dividend payout to reflect the payouts well. Unlike dividend stocks in the US, Singaporeans also don’t have to worry about paying dividend or capital gains tax on their REIT investments – yet. However, depending on the broker used, additional broker / withdrawal fees may apply.)

US Stock Exchange (NYSE / NASDAQ)

To make things easier for our newer investors, there are essentially two markets here (so 3 if you include the crypto market).

With Keppel DC REIT it was listed on the SGX (Singapore Exchange). Our upcoming Tesla stock can be found on the NYSE (New York Stock Exchange).

In essence, the US markets are notorious for their incredible volatility, which makes them an incredibly attractive prospect for day and swing traders alike.

Tesla

It gets a lot easier here.

Though I would have to add currency conversions briefly (excuse the OCD).

Assuming you converted USD 10,000 to USD on February 15, 2019 at the market opening rate of ~ 0.7364, you would have USD 7,364 (S $ 9,723) to play with.

Assuming that you had invested that $ 7,364 in Tesla shares at launch on February 15, 2019, you would have bought a maximum of 120 shares at $ 60.90 each (after the stock split).

This would total ~ $ 7.308USD.

Fast forward 2 years later, and again assuming you sold at the ~ $ 818 market opening price (Feb 16, 2021), you would have amassed a staggering $ 98,160.

Now all you have to do is convert that number back to SGD at the next day’s market opening rate of ~ 1.327 and you have a ridiculous one:

Total = $ 130,258 (1,212.56 percent profit)

Cryptocurrency

Bitcoin, bitcoin, bitcoin.

“This is nonsense.”

“It’s a fraud.”

“Eh … this guy bought bitcoin for $ 3,000. If only I had bought back then ”.

Essentially, think of cryptocurrency as a decentralized, block-chain, virtual currency that is nearly impossible to forge, that cannot (in theory) be tampered with (i.e. printed / changed) by governments – and that is easy to track.

In a way, Bitcoin is similar to gold in the sense that there will ultimately be a limited number of Bitcoins in the world – and thus hedge against inflation.

Of course, this has only been around for a decade, and because of its virtual nature, it has often been touted by many as a speculative good.

Bitcoin

Although it is possible to invest in Bitcoin with SGD, note that only a few “local” brokers (e.g. Coinhako / Binance SG) allow this.

Alternatively, you would have to convert your SGD to USD – which is another hassle.

Assuming that on February 15, 2019, you invested $ 10,000 in Bitcoin at the market price of $ 4,874.22, you could have bought 2 Bitcoins at a price of $ 9,748.44.

Two years fast forward, and assuming you had sold at market price of $ 64,409 on February 15, 2021, you would have amassed:

Total = $ 128,818 (1,221.42 percent profit)

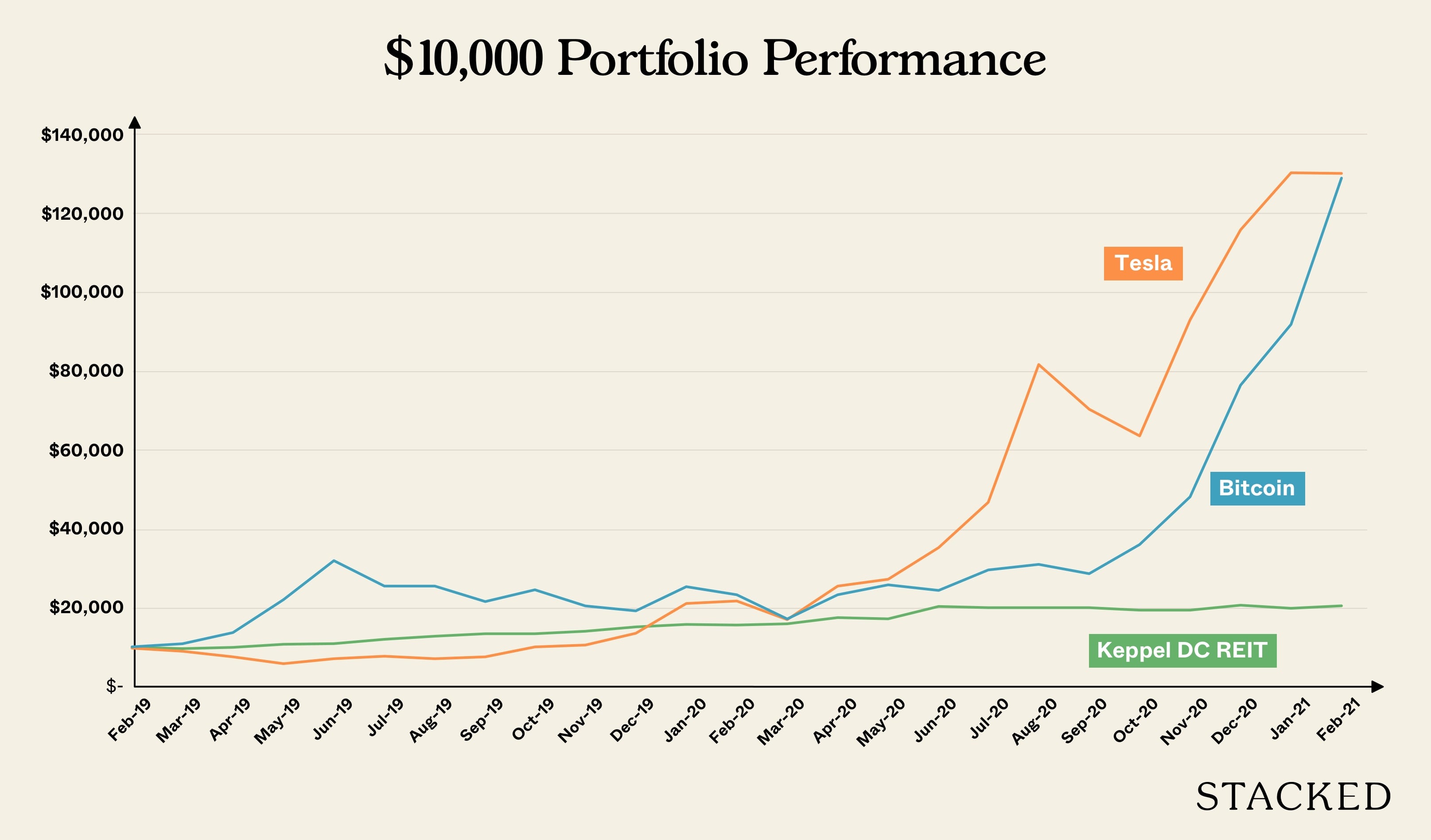

Here is an illustration of what the portfolio would look like in 2 years.

So who is the real winner?

While the Tesla investment ended up having the highest total number (due to the total inventory purchased based on $ 10,000 in capital), Bitcoin generated the largest total profit at an astonishing 1,221.42 percent.

(Again, note that these calculations exclude both brokerage and withdrawal fees, and are actually just a ballpark to show the incredible gains made by these two asset classes.)

The ultimate cherry tree? Indeed.

If you were to look at the returns on the SNP500 and iEdge Reit over the past two years, they would have pales in comparison to the individual asset gains we calculated today.

Note that this does not even reflect the broader market average, but that these are indices that contain a basket of “similar” companies / trusts.

Essentially, this shows that both Tesla and Keppel DC Reit were outliers of their classes during those 2 years.

I’m not going to go into average market profits as this is a whole new ball game – but it’s important to note that not all stocks / speculative assets will produce such returns.

Conclusion (investment tips)

Ultimately, there are tons of investment methods and assets to choose from. Growth, value, dividends, speculative assets – this really is just the tip of the iceberg.

Delving into the pros and cons of each asset now would be a giant wormhole jump. Instead, I’ll close with some investment tips based on the current investment climate:

- “The most dangerous investors are those who have only seen a bull market”.

This age-old adage couldn’t be more fitting for the market exurophy we see today.

Over the past month I’ve heard the same sentence countless times: “Reuben, I’ve earned two years’ salary in less than a year … without doing anything!”

Congratulations!

But the opposite also applies to newcomers – especially those who have invested in speculative assets that have seen massive growth since then.

The solution to all of that?

Invest wisely.

For now, use only 5 to 10 percent of your equity (note: not all of your net worth) on speculative assets – no matter how lucrative they may seem … and be prepared to lose it all.

Remember, it’s always speculation until it’s no more – and for anyone who successfully speculated, 10 others crashed and burned.

TLDR: Review is for those who play it safe. But it is the ones who play it safe who are guaranteed a semblance of stability.

Next, make sure you have long term investments (you never know when the ‘big green days’ will come, and you want to be in the market when it does. Plus, you’ll save a ton of time and headache your ending ).

Third, invest a large part of your portfolio in solid companies with good fundamentals / leadership / prospects. Of course, the current climate has seen the valuation of many such companies soar to ridiculous heights. Therefore it is more important than ever to find the “right entry-level prices” (easier said than done, as I know).

[[nid:517049]]]

Fourth, you have reserves outside of your stock portfolio for up to 6 months of daily spending (personally, I think this rule applies more to singles … which then leads me to my last point).

Assess your position in life – and invest accordingly.

Obviously, assuming you’re just starting out, you’d have the option to play riskier games unlike a family man in his late 40s or even a retiree in his mid-60s who wants stability more than anything.

By riskier games, I mean allocating more capital to individual stocks / ETS than illiquid asset classes (i.e. real estate), taking out larger loans, allocating more wealth to speculative assets, etc.

You always want to have a clear idea of the fixed percentages of your assets that you want to invest – and in which assets.

By following these best practices, if your stocks make a leap into the future, don’t panic and instead increase the Dollar Cost Average (i.e., keep buying lower every two months) for more returns in a few years.

If you’re a new investor just starting out, you should be disciplined adding portions of your salary to your portfolio every month – think of that as a kind of savings plan.

Ultimately, a young investor’s greatest ally is the benefit of time and the incredible effects of compounding.

This article was first published in Stackedhomes.

{kind=link}