To be a millionaire you have to have a high paying job or be a businessman.

At least that’s what we hear generally.

But there are people who have tacitly accumulated wealth despite having a normal job.

Enter Ronald Read.

I recently came across this retired gas station attendant and caretaker who was worth nearly $ 8 million (S $ 10.7 million) after his death.

Morgan Housel’s The Psychology of Money featured the caretaker turned philanthropist, and I was intrigued by his story, which I wanted to dig further.

From humble employee to millionaire

Ronald Read was born in rural Vermont, USA in 1921 to an impoverished farming family.

To get to high school, he walked and hitchhiked over four miles every day.

He joined the US Army during World War II.

After an honorable discharge in 1945, Read returned to Vermont, where he worked as a gas station attendant and mechanic for around 25 years.

[[nid:460787]]]

He then took on a part-time job at JC Penney, where he muddyed for 17 years until 1997.

Read bought a two-bedroom house for $ 12,000 when he was 38 and lived there with his wife and stepchildren.

He died in 2014 at the ripe old age of 92.

It was then that the world learned of his wealth.

In his will, the ex-janitor gave his stepchildren $ 2 million and his local library and hospital $ 6 million.

What we can learn from Ronald Read

A Washington Post article praised Read, saying:

Indeed, there are many personal finance lessons we can learn from Read’s life. Here are a few of them.

Lesson 1: Have a frugal lifestyle

From what I learn, Read liked to live beneath his means, even though he had the money to pamper himself.

He drove a used 2007 Toyota Yaris. His lawyer recalled that despite his millionaire status, he would park his car in parking lots without parking meters, even if it means a longer journey.

He enjoyed an inexpensive breakfast in the café at Brattleboro Memorial Hospital (the hospital to which he had donated his fortune) and moved to a restaurant called Friendly’s as soon as the coffee shop closed.

Even though Read’s denim jacket fell apart, he used a safety pin to fix it and keep it on.

There was once a dinner at Friendly’s that, although Read could not afford to pay for its meal, which the person paid for on Read’s behalf.

My takeaway from the former janitor’s lifestyle is that frugality is something to embrace.

We may not necessarily have to use safety pins to hold up our clothes, but living below our means goes a long way.

Someone who makes a high monthly salary of $ 20,000 but is spending $ 20,001 still has to live from paycheck to paycheck.

Compare this to someone who makes $ 2,000 but uses a measured amount for daily expenses and the rest for investments and emergency savings.

The person who is not earning that much can actually do better many years later.

Lesson 2: only invest your money in things you know

Read has invested in dividend-paying blue chip stocks.

And he only bought companies that he understood, or as Warren Buffett would say, within his sphere of competence.

Read technology stocks that were avoided because he did not understand them. This is an important point. Knowing which stocks to avoid is critical to building long-term wealth.

We can be tempted to buy these hot Reddit stocks at times as everyone around us is buying them.

Or if we don’t get in the cryptocurrency cart, we might look like a fool.

However, it’s okay to miss out on these opportunities if we don’t understand these investments. There are many other ways to grow our money safely.

Read’s previous investments included AT&T Inc., Bank of America Corp., CVS Health Corp., Deere & Company, General Electric Company, and General Motors Company.

Whenever Read received dividend checks, he used them to buy more stocks and keep adding to his fortune.

Here is a snapshot of Read’s 10 largest holdings since his death:

| Companies | Amount (in USD) |

|---|---|

| Wells Fargo | $ 510,900 |

| Procter & Gamble | $ 364,008 |

| Colgate-Palmolive | 252,104 USD |

| American Express | $ 199,034 |

| JM Smucker | 189,722 USD |

| Johnson & Johnson | $ 183,881 |

| VF Corp. | $ 152,208 |

| McCormick | $ 145,055 |

| Raytheon | $ 142,970 |

| United Technologies | 140,880 USD |

Source: The Wall Street Journal

When he died, he owned at least 95 stocks that were spread across many industries such as healthcare, telecommunications, banking, and consumer goods.

If you are intimidated by individual stock picks, you can also look to Exchange Traded Funds (ETFs) or robo-advisors. The key is to only buy investments that you understand.

Who said that easy-to-understand “boring” companies like Colgate-Palmolive don’t make good investments?

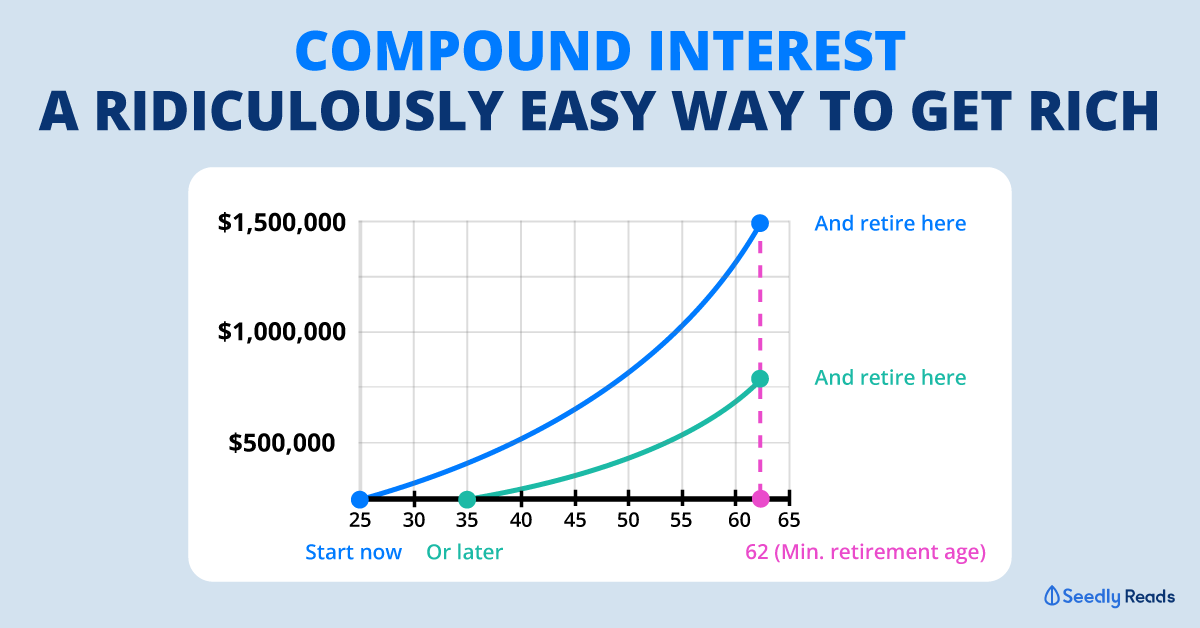

Lesson 3: be patient with your investments

Read is a long-term investor. He understood that compounding takes time to play.

We too can understand the power of compound interest by looking at its formula:

As can be seen, the longer the period n, the more compounding can occur, producing a larger final amount FV.

Read has shown that a long-term investment can really pay off.

Great stuff and great reminder . . . every day! https://t.co/W1sPdnP8ry

— Ronald Read (@RonaldRead18) November 24, 2020

On the contrary, getting in and out of stocks based on trending news will not do our portfolio any good. As the American economist Paul Samuelson once said:

“Investing should be more like seeing paint dry or grass grow. If you want excitement, take $ 800 and go to Las Vegas.”

Lesson 4: be a learning machine

Read was an avid learner.

He read the Wall Street Journal and Barrons, and went to the local public library to check his holdings.

Many successful people acknowledge reading. Apparently, famous investor Warren Buffett reads hundreds of pages every day.

You may not have the patience to go through 500 pages of a book every day, but 10 minutes of reading a day goes a long way. Knowledge connections too.

If you are new to the world of investing, here are 10 books that every beginner should read.

Lesson 5: Mistakes Are Inevitable

Read didn’t always have profit shares.

His portfolio included stocks in Lehman Brothers, the infamous company that went bankrupt in 2008.

However, the collapse did not have a major impact on his returns as his portfolio was diversified.

The lesson here is that we will make mistakes with our investments.

However, the winners should care more than just the losers in a well-built portfolio of high quality companies.

This article was first published in Seedly.

, Cash Information")

{kind=link}